Nobody's Loyal in Aisle Five Anymore

(@munchy_monk)

Post Malone and Megan Trainor canceled their summer concert tours, and some people are saying that live music is dead.

One thoughtful dude by the name of @munchy_monk took this opportunity to explain that the reason live music is hurting is not due to a lack of interest in concerts.

It's because people have no f******g money.

And just like live music, now real estate, travel, hospitality, QSR and health care are all changing because of it.

One place where it is felt most acutely is at the grocery store. So… this is a thought piece on just that. I look at shifts in shopping behavior, the explosive rise of store-brand food, and what different brands can do to meet today’s shopper.

Whether you're the CMO of Red Bull or launching your own artisanal organic hemp-derived cheese puffs brand, what's happening there right now is worth paying attention to, and has an implication for your brand.

The Big Picture: When Money Gets Tight, the Grocery Aisle Splits in Two

Food prices were up 34% over the five years to mid-2025, and with food inflation running at 2.9% through all of 2025 and another 0.5% jump in April 2026, the gap keeps widening.

Most people assume that means everyone's just buying cheaper. The reality is more interesting than that.

Private label (more affordable, store brands) just broke records for the fifth consecutive year. But Premium grocery is growing too. The segment hurting the most is the mainstream, mid-priced branded tier that has defined grocery for thirty years.

Food prices up 34% over five years to mid-2025, 2.9% through 2025, 0.5% in April 2026: Circana via Globe Newswire, August 2025; USDA ERS Food Price Outlook, April 2026; BLS CPI April 2026

This split has precedent. Looking at you, 2008.

In 2008 Flo Rida dropped the hit "Low" and our retirement accounts followed him down. Households couponed, bulk-bought, and discovered the aura of Costco. Some premium products held on… fancy chocolate, single origin coffee, small luxuries that felt like justifiable treats. Economists call it the lipstick effect.

And private label exploded in popularity as people flocked to Walmart-brand this, and Target-brand that.

Fast forward to now. Same movie, different cast.

Private label dollar sales hit a record $282.8 billion for the full year ending December 2025, growing at nearly three times the rate of mainstream middle brands. The Circana CPG Growth Leaders report, which covers 700 manufacturers across every retail channel, tells the rest of the story in one line: super-premium up 7%, premium up 4%, mainstream down 1%, private label up 4%.

Both ends, growing. The middle, squeezed.

Evidence of a K-shaped economy, but also how people decide what they want to buy… regardless of their income.

Private label record $282.8B, national brand unit sales -0.6%: PLMA / Circana Unify+, January 2026

Super-premium +7%, premium +4%, mainstream -1%, private label +4%: Circana 2025 CPG Growth Leaders Report, April 2026

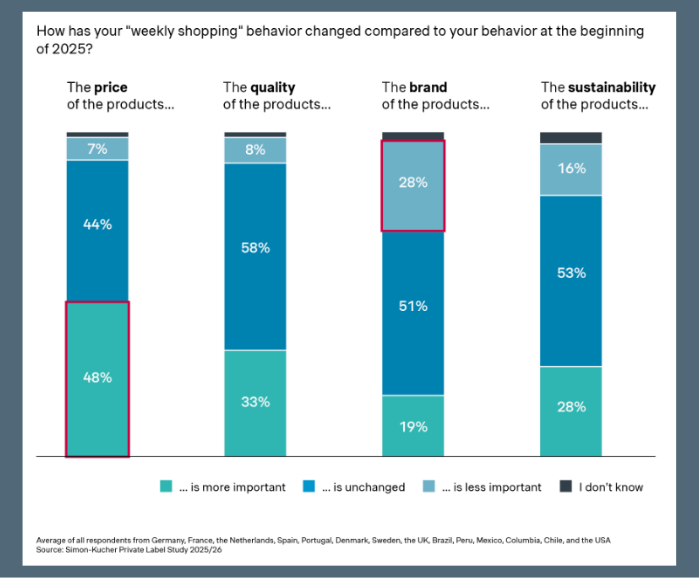

What's different this time: there's no bounce back

(Simon-Kucher Global Shopper Study 2026)

The 2008 recession produced a temporary trade-down. Belts tightened, people switched… but they eventually drifted back to those more expensive middle of the pack favorite brands.

History suggested this one would follow the same arc. Naww, it’s different. Today’s grocery shopper has seen shrinkflation, inflation, and news stories detailing corporate greed on astronomical levels. They approach the grocery store like a battlefield.

In 2024, 71% of consumers said they had noticed shrinkflation. 66% boycotted the product as a result.

Now in 2026, Simon-Kucher's Global Shopper Study of 14,000 consumers show this sentiment has compounded. 57% believe branded products are overpriced without offering a noticeable benefit. 39% describe branding itself as a money-making scheme. And even if prices fall, only a quarter say they would return.

The 25%. That's the number that matters. It's about trust. And trust, once restructured at this scale, doesn't reverse as quickly when the pressure lifts.

71% noticed shrinkflation, 66% boycotted: LendingTree via Packaging Digest, 2024

57% overpriced, 39% money-making scheme, 25% would return: Simon-Kucher Global Shopper Study 2026

Your path to rebuilding trust and winning in 2026 as a food brand depends on where you fall within your category. The top, middle, or bottom.

The bottom: the store brand is the new default

(@michael.discontanzo)

Private label used to be where you went when you couldn't afford the real thing. At parties I’d serve store-brand chips in bowls to avoid being called a cheapo.

That dynamic is different now. Private label is now the rational starting point that everything else has to justify departing from.

This shift is generational and accelerating. Gen Z's share of private label spending is projected to surpass Baby Boomers by mid-2026.

Over 80% of US households earning $100k or more have increased their private label purchases. Walmart's Bettergoods line approached $500 million in its first year. Trader Joe's built an entire brand identity around its own label.

TikTok has accelerated this to Large Hadron Collider speeds. Finding the store brand equivalent of a cult product, filming the comparison, and sharing the verdict is potential virality. The stigma around private label inverted.

For brands in the bottom category of pice, your value got you here. But brand can be what makes someone reach for you twice. How do you elevate beyond a brand concept that’s transactional and low-loyalty into a brand concept that creates distinction? One that doesn’t require implicit price comparison? One with a purpose, story, and identity all your own?

Gen Z private label share projections, 82% of $100k+ households: Numerator via Empower, 2025

Private label $330B, 24% unit share: Circana, March 2026

The middle: the same brand levers face a harder climb

Two signals for the middle of the pack branded tier:

Around half of the world's largest food companies saw volumes decline in the final quarter of 2025, with almost two thirds reporting a drop in earnings compared to pre-Covid levels.

EPS shrank across the mainstream tier in 2025, down 25% for Conagra, 20% for General Mills, 18% for J.M. Smucker, 17% for Kraft Heinz, and 10% for Campbell's. McCormick was the only major food company to post EPS growth.

The mainstream middle isn't losing because the products got worse. It's losing in part because people have been forced to make a more rational calculation in the grocery aisle. “Is this actually worth more than the store brand.”

Cultural presence, emotional heritage, an unhinged Hawaiian Punch mascot… these still matter. But they're working against a greater headwind. A consumer who is more price aware, more label literate, and carrying a low-grade skepticism about whether the extra few bucks is really worth it.

These brands face the greatest risk, and yet they have a brand to build-from. They should look to premium brands for inspiration and guidance on how to break out of this dangerous position. More on that below.

Half of the world's largest food companies saw volumes decline : Dairy Reporter / Food Navigator analysis, April 2026

EPS shrank across the mainstream tier : TD Cowen via Baking Business, February 2026

The top: premium without contradiction

Three price points, which are you buying?

Look at who Circana ranked as its growth leaders in 2025. Chomps ranked second among $500M-$1B brands. Olipop ranked eighth. Pete and Gerry's ranked tenth. Chobani ranked first in the $2.5-$8B tier.

Among other things, what they share is a brand born directly from a product truth.

The ingredient list on Chomps. The nine grams of fiber on Olipop. The pasture-raised, Certified Humane seal on Pete and Gerry's. Chobani doesn't gesture at protein. It tells you how much, in what format, for which occasion.

Great design, clear language, specific positioning, all of it in service of something real. Which is why it lands so differently with a consumer who arrives at the aisle already skeptical.

Now contrast that with the middle. For many of these middle brands, its unclear what makes them a step above private-label. This gap is what's killing the middle mainstream tier.

The brands winning at the top aren't winning because they're spending more. They're winning in part because they have less distance between what they say and what they are.

Chomps #2, Olipop #8, Pete and Gerry's #10, Chobani #1 in tier: Circana 2025 CPG Growth Leaders Report, April 2026

The questions every brand needs to answer

So, how do you respond? It depends on where your brand sits.

If you're at the bottom: Price got you here. But brand is what makes someone reach for you twice. How can you stand for more than “value” and “low cost” and create deeper emotional connections with people? Do you have a story about why you price yourself low? Do you enjoy being a sneaky amazing value?

If you're in the middle: Is your advertising building on something real in the product, or is it being asked to do too much heavy lifting? How can you make the upgrade in price be more felt, seen, and tasted? What brand assets make sense with this evolution? Which are dated?

If you're at the top: Is the gap between you and other tiers felt in the product, visible in the brand, and impossible to ignore at the shelf? Protect your premiumness, and own what sets you apart. Consider what occasions make sense for someone to buy your more expensive, and hopefully-better-quality product.

The market is splitting. It has split before. But this time the consumer isn't just asking whether your product is worth the extra dollar. They're asking whether you're the kind of brand that deserves to charge it.

That's a harder question. And the brands with the clearest answers, and the advertising brave enough to ask it out loud, are the ones pulling away.